Analyzing Cash Receipt Transactions: Cash Discounts

Cash Discounts

To encourage charge customers to pay promptly, some merchandisers offer a cash discount. A cash discount, or sales discount, is the amount that a customer can deduct from the total owed for the purchase, provided the payment is made within a certain time. A cash discount is an advantage to both the buyer, who receives the merchandise at a reduced cost, and the seller, who receives cash immediately.

In general, a cash discount is offered to customers who purchase in bulk and to regular customers. The cash discount may also be offered to get a speedy recovery of money from the charge customer. If the credit terms indicated are 2/10 or n/30 then the customer can deduct two percent from the merchandise cost, provided he pays the whole amount within 10 days; otherwise, he has to pay the full amount or net within 30 days. So 2/10, n/30 means that 2% discount if paid within 10 days, but net is due in 30 days.

Example:

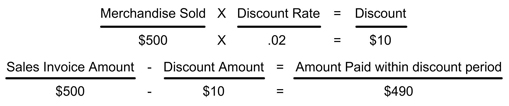

On January 5, 2005, Olympic Sports Wear sold $500 worth of merchandise on account to Franklin High School Athletics. The transaction is recorded as a credit to Sales and a debit to Accounts Receivable for $500. If Franklin High School athletics pays within 10 days (that is, if they make the payment by January 15), then they will get a discount. Hence, Olympic Sports Wear will receive $490 after a discount of $10. The discount can be calculated using the following formula:

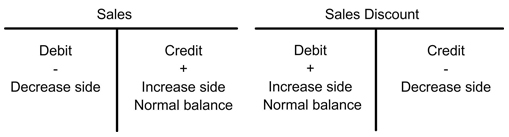

A separate account is used to record cash discounts taken by customers. The $10 discount is entered in the contra revenue account sales discount, which indicates the reduction made in the revenue earned from sales. The normal balance of the sales account is a credit. The normal balance of the sales discount account is a debit.