The Credit Memorandum and Cash Refunds

If the sales return or allowance occurs on a charge sale, the business usually prepares a credit memorandum. A credit memorandum lists the details of a sales return or allowance. The charge customer’s account is credited (decreased) for the return amount or allowance.

Journalizing a Credit Memorandum

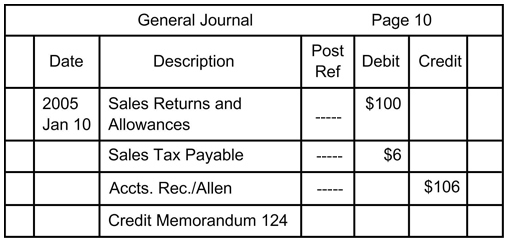

On January 10, 2005, Olympic Sports Wear issued credit memorandum 124 to Allen for the return of merchandise purchased on account: $100 plus $6 sales tax.

Identify

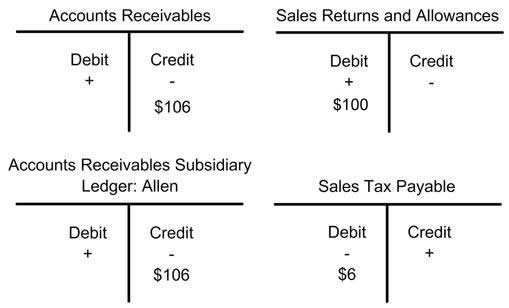

The accounts affected are Accounts Receivable (controlling), Accounts Receivable: Allen (subsidiary), Sales Returns And Allowances, and Sales Tax Payable.

Classify

Accounts Receivables (controlling) and Accounts Receivables: Allen (subsidiary) are asset accounts. Sales Returns and Allowances is a contra revenue account. Sales Tax Payable is a liability account.

Analyze

Sales Returns and Allowances are increased by $100. Sales Tax Payable is decreased by $6. Accounts Receivable (controlling) and Accounts Receivable: Allen (subsidiary) are decreased by $106.

Apply Debit Rule:

Increases to a contra revenue account are recorded as debits. Debit Sales Returns and Allowances for $100. Decreases to liability accounts are recorded as debits. Debit Sales Tax Payable for $6.

Apply Credit Rule:

Decreases to asset accounts are recorded as credits. Credit Accounts Receivable (controlling) and Accounts Receivables: Allen (subsidiary) for $106 each.

This is how the transaction would appear if T-Accounts were used. Remember that T-accounts are only used to visualize the debit and credit sides of a transactionthey are not formal accounting forms and are not used for recording/journalizing transactions. In Unit 4, you learned about recording transactions in a General Journal, which is shown below the T-accounts.:

Make a Journal Entry and then post. Transactions are recorded in a journal, and then posted from the journal to the ledger. A journal is a book of transactions; a ledger is a book of accounts and their balances.

Posting transactions to the accounts receivable subsidiary ledger:

- The credit is to Accounts Receivable: Allen.

- The slash indicates that both Account Receivable (controlling) and Accounts Receivable (subsidiary) have been credited.

- Please note that a diagonal line is entered in the Post Ref. column. This diagonal line indicates that an amount, $106, is posted in two places: first to the Accounts Receivable (controlling) account in the general ledger, and then to the Allen account in the Accounts Receivable subsidiary ledger.

- After the amount is posted to the Accounts Receivable (controlling) account, the account number is entered to the left of the diagonal line in the posting reference column.

- After the amount is posted to the subsidiary ledger account, Allen, a check mark is entered to the right of the diagonal line.

The various accounts involved in posting to the accounts receivable subsidiary ledger are:

- General Journal Entry (This is how this transaction would appear in the General Journal)

Post from the above General Journal into Ledger accounts, so that account balances can be determined.

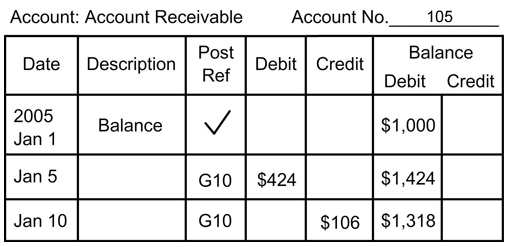

- Ledger - Accounts Receivable (Notice how the account balance is decreased by a return)

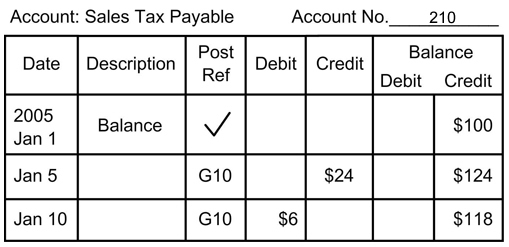

- Ledger - Sales Tax Payable (Notice how the account balance is decreased by a return)

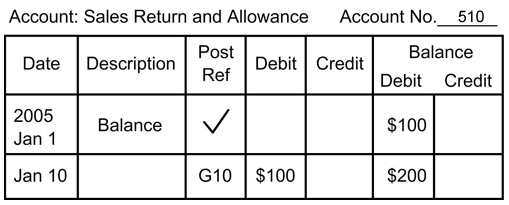

- Ledger - Sales and Return Allowances (You are increasing the amount of Sales Returns; so this account balance increased.)