Recording a Sale on Account

According to the revenue recognition principle, revenue for a sale on account is recognized and recorded when the sale is earned. Revenue must also be realizable, which means that it is expected to be converted to cash.

Below is a typical business transaction:

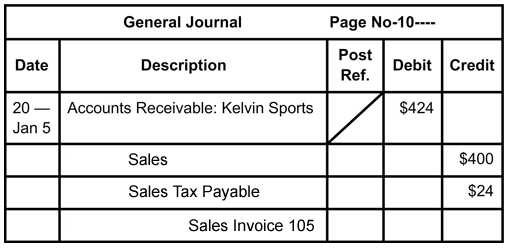

On January 5, 2005, Olympic Sports Wear sold merchandise on account to Kelvin Sports for $400 plus $24 in sales tax, with sales slip number 105.

Identify:

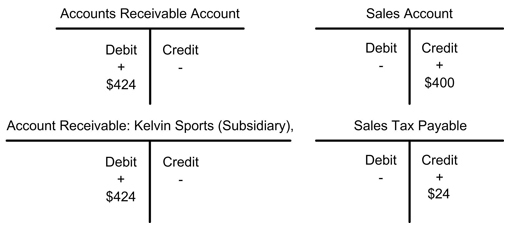

The accounts affected through this transaction are Accounts Receivable (controlling), Accounts Receivable: Kelvin Sports (subsidiary), Sales, and Sales Tax Payable.

Classify:

Accounts Receivable (controlling) and Accounts Receivable: Kelvin Sports (subsidiary) are asset accounts, Sales is a revenue account, and Sales Tax Payable is a liability account.

Effects:

Accounts Receivable (controlling) and Accounts Receivable: Kelvin Sports (subsidiary), increase by $424. Sales increases by $400 and Sales Tax Payable increases by $24.

Apply Debit Rule:

Increase to asset accounts are recorded as debit. Accounts Receivable (controlling) and Accounts Receivable: Kelvin Sports (subsidiary) are debited.

Apply Credit Rule:

Increases to revenue and liability accounts are recorded as credit; credit Sales for $400 and Sales Tax Payable for $24

This is how the transaction would appear if T-Accounts were used. Remember that T-accounts are only used to visualize the debit and credit sides of a transactionthey are not formal accounting forms and are not used for recording/journalizing transactions. In Unit 4, you learned about recording transactions in a General Journal, which is shown below the T-accounts.

Prepare a Journal Entry:

The journal entry for the transaction is show below (Remember that the debit account is always listed first):

After this entry is journalized in the journal, the debits and credits would then be posted to individual ledger accounts. Page 13 shows examples of ledger accounts and account balances.