Sales Returns and Allowances

Sometimes, customers may be dissatisfied with their purchases due to damage or defect. In such cases, merchants allow them to return the merchandise. Any merchandise returned for credit or a cash refund is known as a sales return. A price reduction granted to the customer for damaged goods is known as a sales allowance.

Sales returns and allowances summarize the total returns and allowances for damaged, defective, or otherwise unsatisfactory merchandise. If the sales returns and allowances account balance is larger than the sales account balance, there may be problems with merchandising.

Sometimes a merchant will give a customer a cash refund instead of a credit. For cash refunds, the cash in bank account is credited instead of accounts receivable.

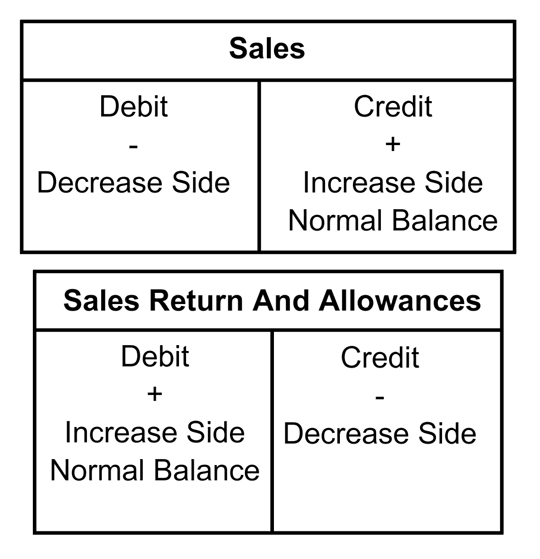

Sales Returns and Allowances Accounts:

The sales returns and allowances account is a contra account. The balance of the related account decreases with the contra account. Sales returns and allowance is more specifically classified as contra revenue account because it is related to a revenue account - sales. The normal balance side of sales is a credit and the normal balance side of sales return and allowances is a debit.