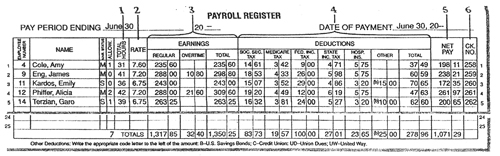

Purpose of Payroll Records

A payroll record is produced at the end of each pay period, and shows a list of employees who have been paid.

The contents of the record are:

- Warrant or ACH number

- Employee names

- Detail of earnings

- Deductions/allowances/reimbursements

- Net pay

The details of the other sections are explained below.

- Total Hours Column – The total number of regular and overtime hours from the employee’s time card appears here.

- Rate Column – The employee’s current rate of pay (from the employee’s earnings record) appears here.

- Earnings Section – This section has three sub-columns:

- Regular

- Overtime

- Total earnings

- Deduction Section – The number of sub-columns in this section varies from business to business. For example, it may contain:

a) Social Security tax

b) Medicare tax

c) Federal Income tax

d) State Income tax - Net pay column – Net pay is the amount left after total deductions have been subtracted from gross earnings.

- Check number column – The check number issued appears in this column.

- Column totals – Each column is totaled, and the totals appear on the last line of the payroll register.

The employees’ earnings record:

In addition to the payroll register, businesses should maintain an earnings record for each employee. This record contains all the payroll information related to an employee.

The earnings record and the payroll register have the same columns:

- Three earnings columns

- Four columns for deductions required by law

- Additional columns for voluntary deductions

- The total column

- The net pay column

There should also be one additional column for the employee’s accumulated earnings, showing the employee’s year-to-date gross earnings.