Income Tax and Exemptions

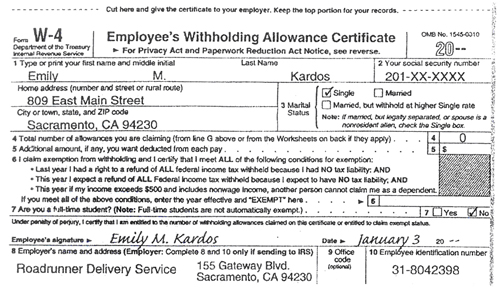

Federal and state income taxes are required deductions under federal and state law. Taxes are withheld from each payroll check in accordance with the gross pay per check and the number of exemptions claimed on the employee's W-4 Withholding Exemption Certificate. Until an employee files a W-4 with the payroll department, the maximum deduction will be withheld, in accordance with the law.

Any change in exemptions requires that a new W-4 be submitted to the payroll department. W-4 forms can be obtained from the payroll department, or an employer may keep a supply on hand.

Clauses of Income Tax Deductions:

- A taxpayer is usually allowed one personal allowance and one allowance for each person he or she supports.

- Some employees are exempted from federal income tax withholding. An employee is not required to have income tax withheld if he or she:

- did not have a federal income tax liability in the previous year

- expects no tax liability this year

- has income of $700 or less including non-wage income such as savings account interest

- cannot be claimed as a dependent on someone else’s tax return.