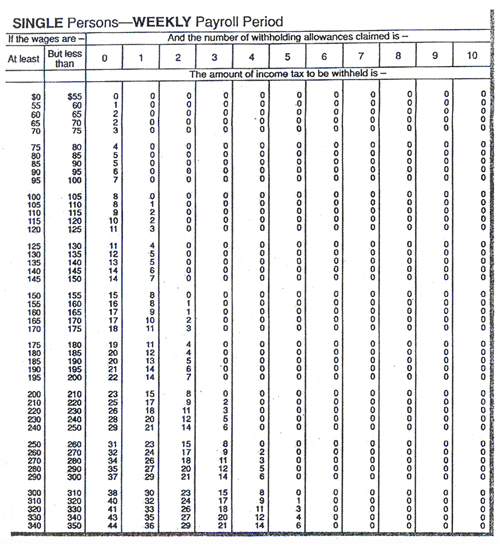

Social Security and Medicare Taxes

In the United States, employers are required to withhold federal income tax, plus one half of the Social Security tax and one half of the Medicare tax. Together, the employer and employee's shares of the Social Security and Medicare taxes are known as the FICA tax. In some places, employers may be required to withhold State Income tax, or even City Income tax in addition to the above requirements.

Federal law requires deductions for Social Security. A percentage of pay (as determined by the Social Security Act) is withheld from each paycheck. In addition, employers are required to contribute an equal amount for future Social Security retirement and/or disability benefits.

Social Security contributions are recorded and reported by each employee's Social Security number and it is therefore critical that paychecks reflect these accurately.

Social Security tax fund programs provide income to the following individuals:

- The old age and disability insurance programs provide income to retired or disabled people and their dependent children.

- The survivors’ benefits program provides income to the spouse and dependent children of a injured worker.

Employees who are exempt from federal income taxes are generally still subject to FICA taxes. The FICA tax rates are as follows:

| Social Security tax | 6.20% |

| Medicare tax |

1.45% |

| Total FICA taxes | 7.65% |

The Social Security tax is deducted from the employee’s earnings until the maximum taxable earnings amount for the year is reached (this amount increases each year). For 2007, the maximum taxable earnings amount was $97,500.