Detecting Errors in the Subsidiary Leger

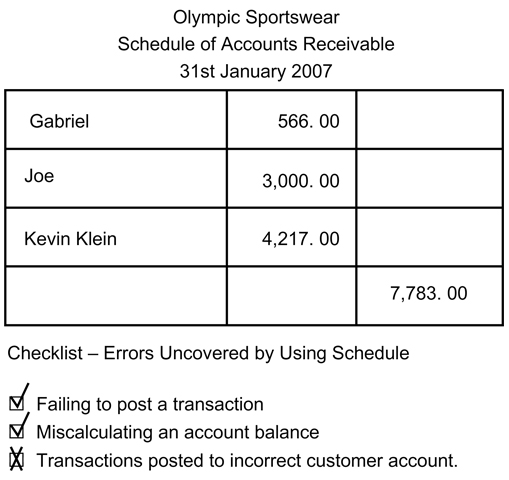

Proving the Accounts Receivable Subsidiary Ledger with the controlling account verifies that the sum of the subsidiary ledger equals the controlling account’s ending balance. This internal control procedure uncovers errors such as failing to post a transaction, or miscalculating an account balance.

This action, however, does not ensure that transactions are posted to the correct customer account. The subsidiary ledger and the controlling account may balance even if an amount was posted to the wrong account. This type of error is often discovered when a customer finds the error on a bill and reports it.