Journalizing Payroll Liabilities - Example

Follow the steps below to journalize payroll entries.

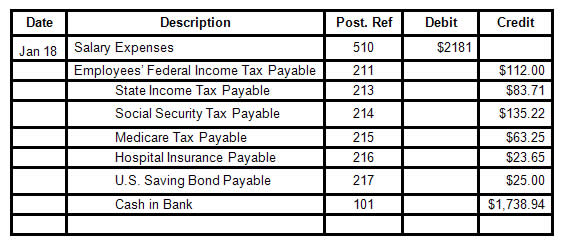

The payroll register of John Roadways is the source document for the payroll journal entry.

- Identify: The following accounts are affected:

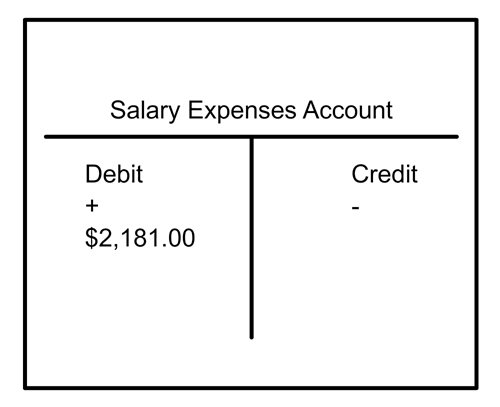

- Salaries Expense

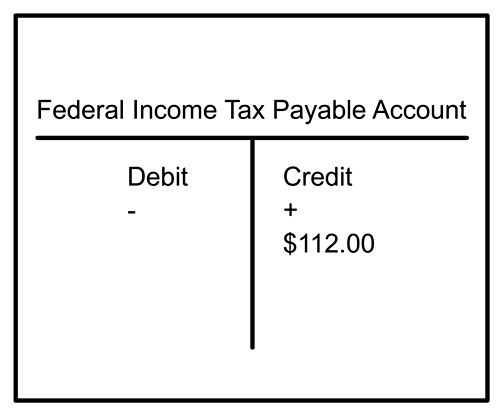

- Employees’ Federal Income Tax Payable

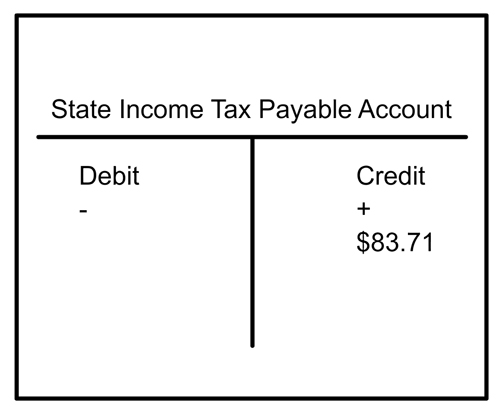

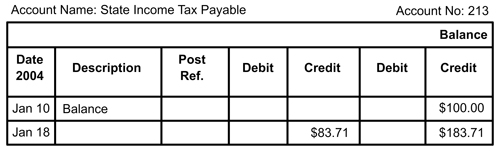

- Employees’ State Income Tax Payable

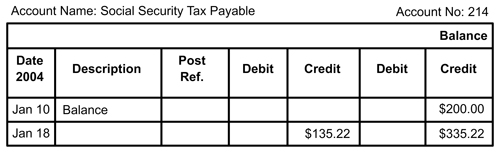

- Social Security Tax Payable

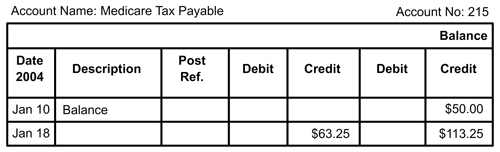

- Medicare Tax Payable

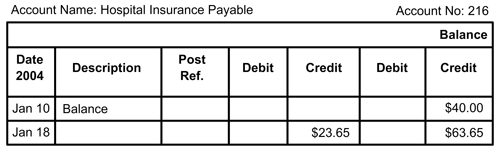

- Hospital Insurance Payable

- U.S. Savings Bonds Payable

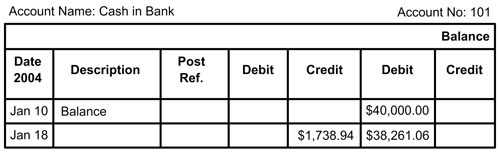

- Cash in Bank

- Classify: The accounts are classified as:

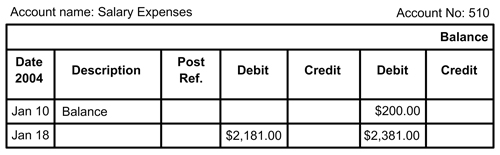

- Salaries Expense - Expense Account

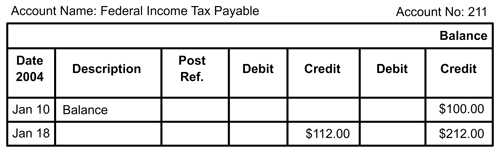

- Employees’ Federal Income Tax Payable - Liability

- Employees’ State Income Tax Payable - Liability

- Social Security Tax Payable - Liability

- Medicare Tax Payable - Liability

- Hospital Insurance Payable - Liability

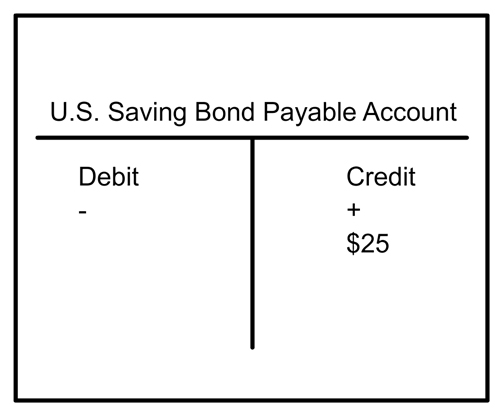

- U.S. Savings Bonds Payable - Liability

- Cash in Bank – Asset Account

- Effect: The effect on the accounts is:

- Salaries Expense account increased by $2,181.00

- Employees’ Federal Income Tax Payable increased by $112.00

- Employees State Income Tax Payable increased by $83.71

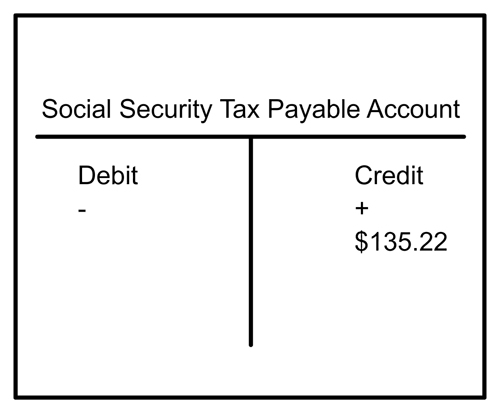

- Social Security Tax Payable increased by $135.22

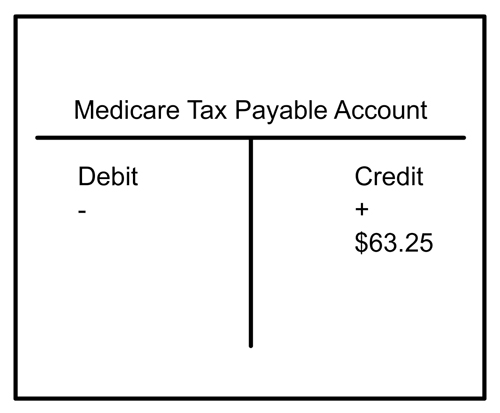

- Medicare Tax Payable increased by $63.25

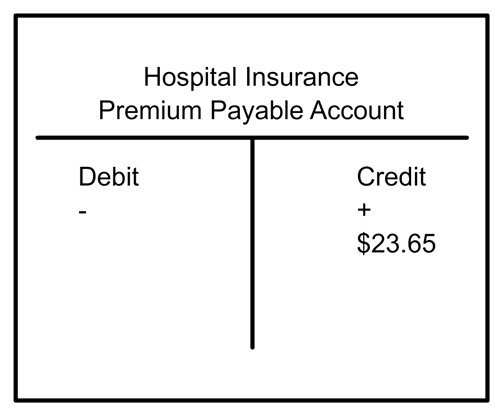

- Hospital Insurance Payable increased by $23.65

- U.S. Savings Bonds Payable increased by $25.00

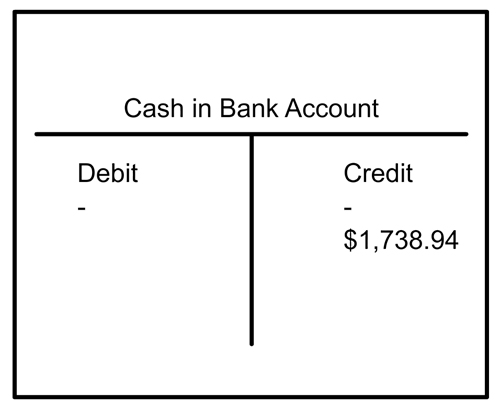

- Cash in Bank decreased by $1,738.94

- Debit rule: Debit Salaries Expense account

- Credit rule:

- Credit all liability accounts (Federal Income Tax Payable, Employees’ State Income Tax Payable, Social Security Tax Payable, Medicare Tax Payable, Hospital Insurance Payable, U.S. Savings Bonds Payable)

- Credit Cash in Bank (asset account decreases)

- Prepare T Accounts

- Post the payroll entry:

The following table shows the general journal entry and the individual ledger accounts after posting:

Journal entry:

Ledger Accounts:

Salaries Expenses:

Federal Income Tax Payable:

State Income Tax Payable:

Social Security Tax Payable:

Medicare Tax Payable:

Hospital Insurance Payable:

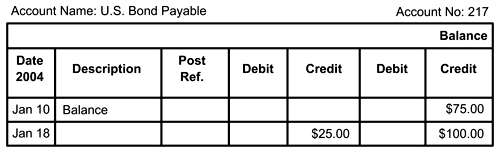

U.S. Savings Bonds Payable:

Cash in Bank: