Preparing Payroll Tax Forms

Employers complete many different types of payroll-related tax forms.

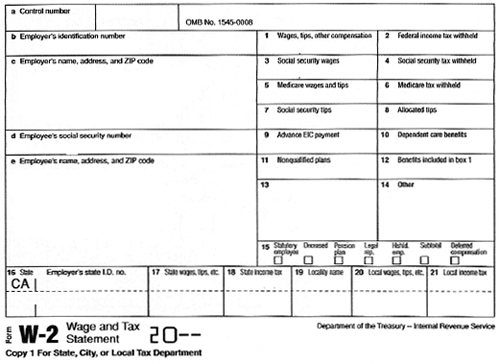

Form W–2 gives a summary of an employee’s earnings and withholdings for the calendar year. It includes the following:

- Gross earnings

- Federal income tax withheld

- FICA taxes withheld

- State and local income taxes withheld.

Employees receive Form W–2 by January 31st of the following year, and use it to prepare their individual income tax returns. Employers prepare several copies of Form W-2 for their employees in order to help them prepare their individual income tax returns: one copy is for the IRS, one for the employee, and one for the employer’s records. Additional copies are sent to city or state government, if necessary.

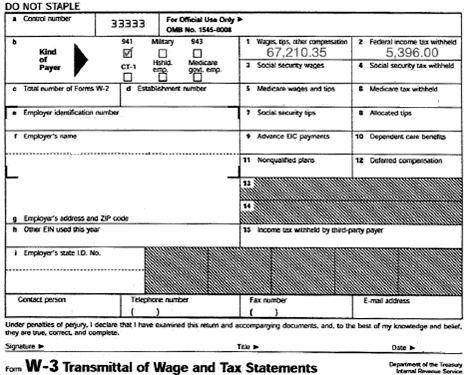

Along with the Form W-2, the employer files Forms W-3, Transmittal of Wage, and Tax Statements with the federal government. Form W-3 explains the information on the Form W-2. Both forms are due by February 28.

The federal government uses the Form W-2 information to check individual income tax returns. The sample copy of Forms W-2 and W-3 are shown below:

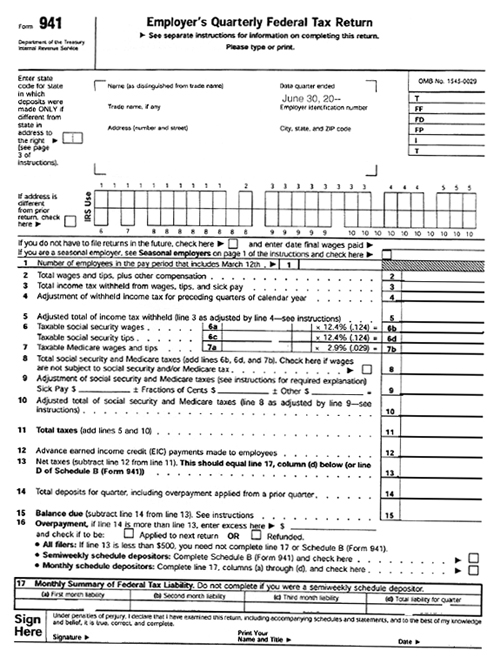

Forms 941 and 940:

Form 941 is the employer’s quarterly Federal Tax return. It reports accumulated amounts of FICA and Federal Income Taxes withheld from employees’ earnings, as well as FICA tax owed by the employer. The employer’s federal unemployment tax is reported annually on Form 940.