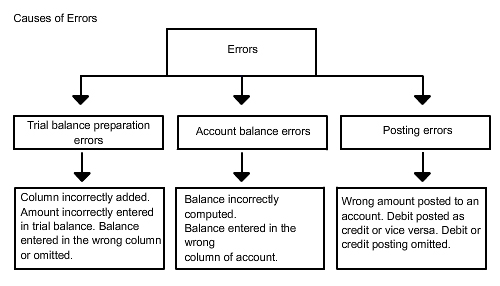

Cause of Errors

It is important to be careful when recording transactions in the journal and posting them into ledger accounts. If errors do occur in the accounts, they can be discovered either through audit procedures or by looking at the trial balance.

If the two trial balance totals are not equal, the difference in the total should be determined before searching for the error.

In many cases, the difference between the two totals of the trial balance gives a clue about the nature of the error, or where it occurred.

For example, a difference of 10, 100, or 1,000 between two totals is often the result of an error in addition.

A difference between totals can also be due to the omission of a debit or a credit posting. If the difference can be evenly divided by two, the error may be caused by posting a debit as a credit, or vice versa.

For example, if the debit total is $20,640 and the credit total is $20,236, the difference would be $404. This may indicate that a credit posting of $404 was omitted, or that a credit of $202 was incorrectly posted as a debit.

Two other common types of errors that occur are known as transpositions and slides.

A transposition occurs when the order of the digits is mistakenly changed. An example of this could be to write $542 as $452 or $524. In a slide error, the entire number is mistakenly moved one or more spaces to the right or the left. This could change $542.00 to $54.20 or $5,420.00.

If an error of either type has occurred and there are no other errors, the difference between the two trial balance totals can be evenly divided by nine.

If an error is not revealed by the trial balance, the steps in the accounting process must be retraced, beginning with the last step and working back to the entries in the journal. (Usually, errors causing the trial balance totals to be unequal are discovered before all of the steps are retraced.)