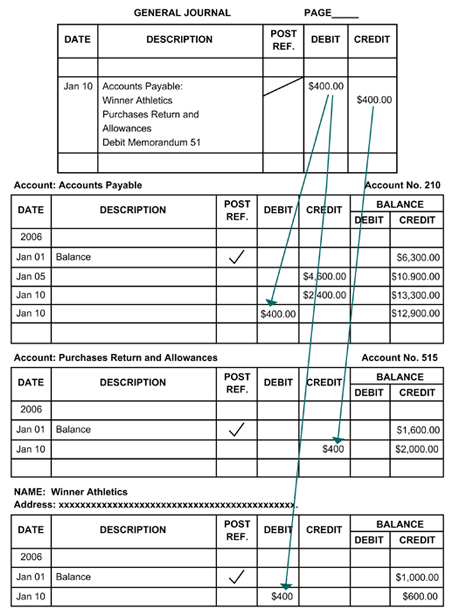

Recording Purchasing Returns and Allowances

The following example illustrates the procedure for recording a purchasing return transaction:

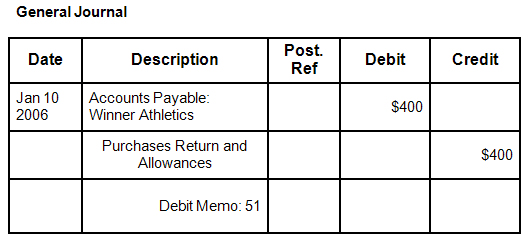

On January 10, Olympic Sports Wear issued debit memorandum 51 for the return of $400 in merchandise purchased on account from Winner Athletics.

Step 1: Analysis

- Identify: The accounts affected are Accounts Payable (controlling), Accounts Payable: Winner Athletics (subsidiary), and Purchases Returns and Allowances.

- Classify: Accounts Payable (controlling) and Accounts Payable: Winner Athletics (subsidiary) are liability accounts. Purchase Returns and Allowances is a contra cost of merchandise account.

- Effects: Accounts Payable (controlling) and Accounts Payable: Winner Athletics (subsidiary) are decreased by $400. Purchases Returns and Allowances is increased by $400.

Step 2: Debit – Credit Rule:

- Decreases to liability accounts are recorded as debits. Debit Accounts Payable (controlling) for $400, and Debit Accounts Payable: Winner Athletics (subsidiary) for $400.

- Increases to contra cost of merchandise accounts are recorded as credits. Credit Purchases Returns and Allowances for $400.

Step 3: Make a Journal Entry

Posting to the Accounts Payable Subsidiary Ledger

The $400 debit is posted to two accounts of Winner Athletics:

- The Accounts Payable controlling account

- The Accounts Payable subsidiary ledger account

After the entry is posted to Accounts Payable, the account number 210 is entered to the left of the diagonal in the Posting Reference column. After the amount is posted to Winner Athletics, a check mark (√) is entered to the right of the diagonal line.