Merchandising Purchasing on Account

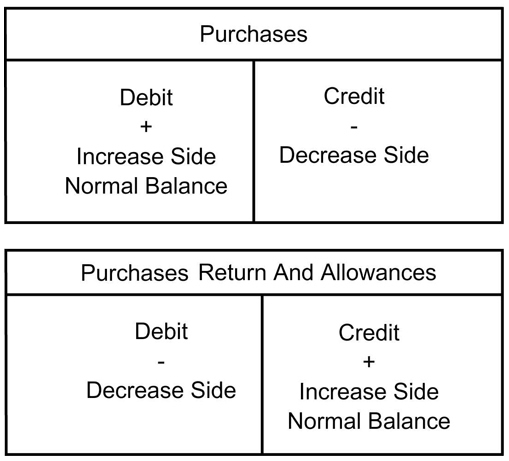

Purchasing Returns and Allowances

A purchase return occurs when a business returns merchandise to the supplier for full credit.

A purchase allowance occurs when a business keeps less than satisfactory merchandise and pays a reduced price.

The Purchase Return and Allowances Accounts is used to record the return of merchandise to a supplier or to record an allowance. It is classified as a contra cost of merchandise account to the purchase account. The normal balance of Purchases Account is debit; thus, the Purchase Returns and Allowances Account has a credit balance.

Details related to debit and credit for this account are listed below:

- A debit memorandum (or memo) is used to notify suppliers (creditors) of a return or to request an allowance.

- The “debit” in debit memorandum indicates that the creditor’s account will be debited, or decreased.

- A debit memorandum always results in a debit (decrease) to the accounts payable controlling account in the general ledger, and to the creditor’s account in the subsidiary ledger.

- The account credited depends on whether the debit memorandum is for merchandise or another asset.

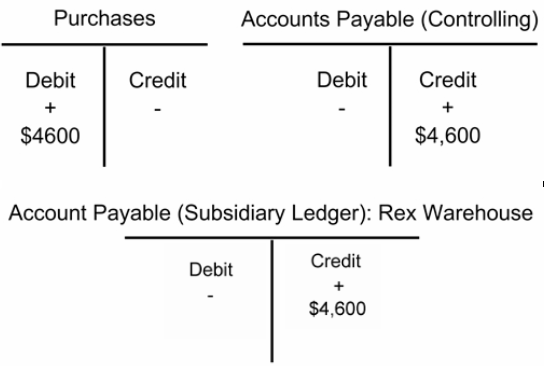

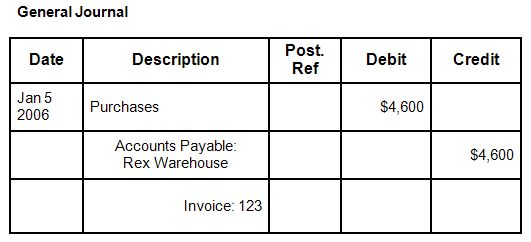

Example 1:

The following example illustrates the purchasing details of Olympic Sports Wear. The merchandise purchase amount is $4,600, on account from Rex Warehouse; invoice no. 123.

Step 1: Analysis

- Identify: The accounts affected are Purchases Account, Accounts payable (controlling), Accounts Payable: Rex Warehouse (Subsidiary).

- Classify: Purchases Account is a cost of merchandise account. Accounts Payable (controlling) and Accounts Payable: Rex Warehouse (Subsidiary) are liability accounts.

- Effects: Purchases Account is increased by $4,600. Accounts payable (controlling), and Accounts Payable: Rex Warehouse (Subsidiary) are increased by $4,600 each.

Step 2: Debit – Credit Rule:

- Increases to cost of merchandising are recorded as debit. Debit Purchases Account $4,600.

- Increases to liability account are recorded as credit. Credit Accounts payable (controlling) and Accounts Payable: Rex Warehouse (Subsidiary) for $4,600 each.

Step 3: Prepare a T Account:

Step 4: Make a Journal Entry

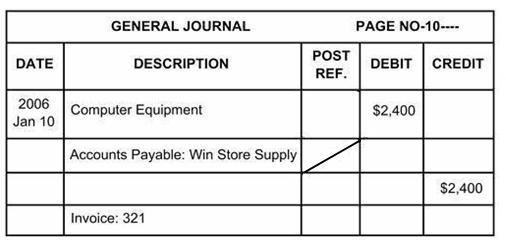

Example 2:

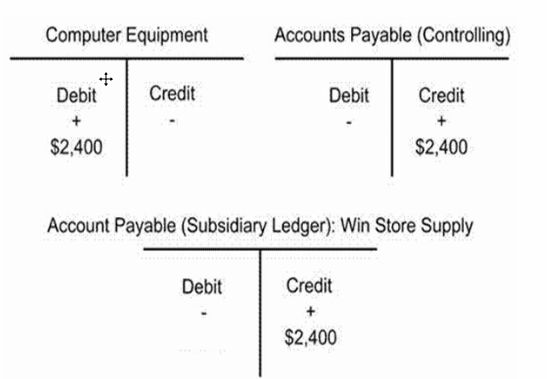

This example illustrates the purchase details of Olympic Sports Wear. The company purchased computer on account for $2,400 from Win Store Supply on account, invoice number: 321.

Step 1: Analysis

- Identify: The accounts affected are Computer Equipment Account, Accounts Payable (controlling), and Account Payable: Win Store Supply (Subsidiary).

- Classify: Computer Equipment is an asset account. Accounts Payable (controlling) and Account Payable: Win Store Supply (Subsidiary) are liability accounts.

- Effects: Computer Equipment is increased by $2,400, Accounts Payable (controlling), Account Payable: Win Store Supply (Subsidiary) are increased by $2,400.

Step 2: Debit – Credit Rule:

- Increases to asset accounts are recorded as debit. Debit Computer Equipment $2,400

- Increases to liability accounts are recorded as credit. Credit Accounts Payable (controlling) and Account Payable: Win Store Supply (Subsidiary) for $2,400 each

Step 3: Prepare a T Account

Step 4: Make a Journal Entry