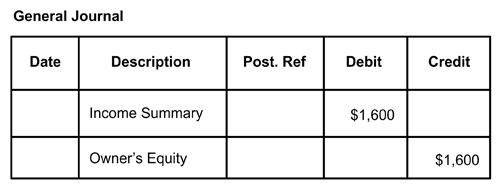

Closing Income Summary to Capital

This is the third closing entry. It involves transferring the balance of the income summary account to the capital (or) owner’s equity account.

To better understand this step, observe the following example:

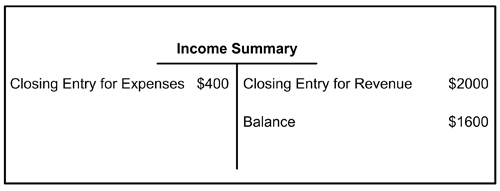

After closing the revenue and expenses accounts, the income summary has a credit balance of $1,600.

Step 1: Analysis

- The Income Summary and Capital Account are affected.

- Income Summary is a temporary Owner’s Equity Account. Capital is an Owner’s Equity Account.

- By transferring $1,600, the balance of the Income Summary is reduced to zero. By transferring the Net Income amount to the Capital account, the Capital increases by $1,600.

Step 2: Debit – Credit Rule

a. To reduce the income summary balance to zero. Debit Income summary for $1,600.

b. Net income is recorded as a credit to the Owner’s Capital account. Credit Owner’s Capital for $1,600.

Step 3: Make a Journal Entry