Learn

Vocabulary

Supply and Demand

The problems you will see in relation to supply and demand will require you to start with a product at equilibrium. To do this draw, a supply and demand graph and label the equilibrium price and equilibrium quantity.

Remembering the non-price determinants for both supply and demand (TRIBE and ROTTEN), you will be asked to determine which curve is moving, which direction it is moving, and what happens to the equilibrium price and quantity.

Demand and Supply Together = Market Equilibrium

Open Market Equilibrium in a new tab

The intersection of the supply and demand curves determines the market equilibrium. At the equilibrium price, the quantity demanded equals the quantity supplied. In market economies, prices are the signals that guide economic decisions and thereby allocate scarce resources.

- For every good in the economy, the price ensures that supply and demand are in balance.

- The equilibrium price then determines how much of the good buyers choose to purchase and how much sellers choose to produce.

- The price is determined when buyers and sellers interact in the marketplace.

- The behavior of buyers and sellers naturally drives markets toward their equilibrium.

- When the market price is above the equilibrium price, there is a surplus of the good, which causes the market price to fall. When the market price is below the equilibrium price, there is a shortage, which causes the market price to rise.

If demand exceeds supply, shortages result. If supply exceeds demand, surpluses result. Market equilibrium results when demand equals supply. The definition of equilibrium is when there are no surpluses or shortages in the marketplace.

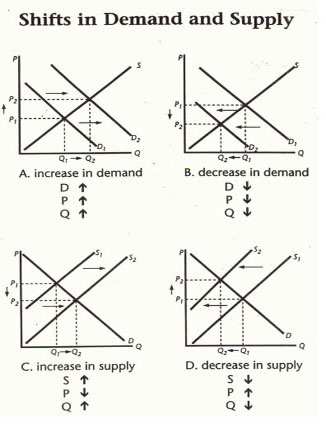

To analyze how any event influences a market, we use the supply-and-demand diagram to examine how the event affects equilibrium price and quantity. To do this we follow four steps:

STEP 1: Draw a graph that shows price on the vertical axis and quantity demanded and supplied on the horizontal axis. Draw a giant X. Label your two curves correctly, D and S. Circle the equilibrium point on this graph.

STEP 2: Decide whether the event shifts the supply curve or the demand curve (or both). Draw a new curve and circle the new equilibrium point.

STEP 3: Compare the new equilibrium with the initial equilibrium by 'reading' your graph. Did price increase or decrease? Did quantity demanded and supplied increase or decrease?

When only a single curve is shifting, there are only four possible ways the graphs and equilibrium point can change.

Open Demonstrating Graphing Equilibrium with One Shift in a new tab

STEP 4: Wow! What if BOTH supply and demand curves shifted? This will signal to you that EITHER equilibrium price OR equilibrium quantity will be indeterminate. This means that one of these cannot be determined given that we do not know the extent of the shift in the marketplace.

Open Demonstrating Graphing Equilibrium with Simultaneous Shifts in a new tab

Too High or Too Low?

What happens when the market does not have the right price? Sometimes the price of a product can be too high or too low.

- According to the Law of Demand, if the price of a product is too high, consumers will buy less of it. So, there is a surplus of the product.

- To motivate consumers to buy the product, producers will have to lower its price. According to the Law of Demand, as the price of a product decreases, consumers will buy more of it.

- However, according to the Law of Supply, as the price of a product decreases, producers will offer less of it for sale. This lowering of the price will occur until equilibrium is reached.

What if the market price for a product is too low?

- Remember, according to the Law of Supply, as the price of a product decreases, producers will offer less of it for sale.

- However, according to the Law of Demand, as the price of a product decreases, consumers will want to buy more of it.

- So, there will be a shortage of the product.

In a shortage situation, stores won't be able to keep it in stock. In order to get the product, consumers will have to bid up its price.

- According to the Law of Demand, as the price of a product increases, consumers will want to buy less of it.

- However, according to the Law of Supply, as the price of a product increases, producers will want to offer more of it for sale.

- This rising of price will continue until the equilibrium price is reached.

A market economy is said to be very efficient because the tendency will be for the market to gravitate towards equilibrium.

Constructing Ceilings and Floors

Sometimes the government tries to help certain groups of people by changing the price of an item. Through legislation, government will artificially set the price for the item by setting price floors and price ceilings.

Price floors and price ceilings are opposite of what we would likely think these words mean.

- Floors are above equilibrium, with supply exceeding demand (minimum wage).

- Ceilings are below equilibrium, with demand exceeding supply (like gas in the 1970's and rent-controlled apartments in New York City).

Sometimes the government sets a legal minimum price above equilibrium. This is called a price floor because the government will allow the price to go above the price they set, but they will not allow the price to go any lower.

When the government wants to set a low price below equilibrium, they are establishing a price ceiling. The government will allow the price to go lower than a ceiling, but it cannot go any higher.

All told, Adam Smith Classical, Laissez-Faire Economist prefers that the market resolve the failures, but clearly sometimes government must intervene.

With government intervention, however, results are often less than desirable. When the government does this they are not allowing the market to correct itself and reach equilibrium.

For example: price floor...supply exceeds demand...surplus occurs...and if minimum wage is the example, workers are plentiful but employers do not demand employees at the high wage. If they do, they select only the best, thereby discriminating against the very people the program was designed to help.

For price ceilings...demand exceeds supply...shortage occurs...and if gasoline will not be able to go higher than a set amount then suppliers do not open their gas stations. Remember, suppliers are motivated by high prices, not low prices. Ask your family members about long gas lines in the 1970s!

Open Ceilings and Floors in a new tab

Price Control Chart

| Type of Price Control | Definition | Example | Why is it Instituted? | Possible Unintended Consequences |

|---|---|---|---|---|

| Price Ceiling | A legal maximum that a business can charge for a good or service | Rent controlled apartments in New York City; gasoline in the 1970s | The only way for many people to afford to live in NYC is to have inexpensive rent. Having people live in the city would be good for the cities continued growth, so many apartments have limits on how much the rent can be. Regarding gas in the 1970s, President Nixon felt that the price of gas was getting too high for people to afford.So, he instituted a cap or ceiling on the price of gas. |

A shortage results in a market because fewer apartments are built and those that are may be left in disrepair. Remember, suppliers are motivated by high prices. For gas, long lines resulted to get the cheaper gas. However, the lines weren't because there wasn't gas, it was because suppliers did not keep their stations open throughout the day. |

| Price Floor | A legal minimum that a business can charge for a good or service | Minimum wage | A person deserves a wage that is high enough to maintain a household | A surplus results in the market because businesses hire fewer workers at the high wage. Yes, you are excited about the high wage but suppliers are not. Unfortunately when there is a surplus of workers, employers are able to choose among a large talent pool; when this occurs, the very groups minimum wage is designed to help may be discriminated against. |