Posting Cash Payment Journal

The following types of transactions can be posted to a Cash Payment Journal:

- Posting from the Cash Payments Journal

- Posting the Cash Payment Journal to a Ledger Account

- Posting from the General Debit Column

- Totaling, Proving, and Ruling the Cash Payments Journal

- Posting Column Totals to the General Ledger

- Proving the Accounts Payable Subsidiary Ledger

- Proving Cash

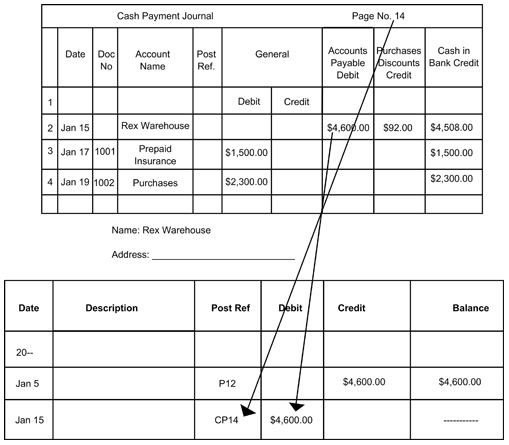

Posting from the Cash Payments Journal

Individual amounts in the Accounts Payable Debit column and the General Debit column are posted at the end of the month. To keep creditor’s account current, clerks make daily posting from the Accounts Payable Debit column to the Accounts Payable Subsidiary Ledger.

Example 1: The following journal illustrates the steps to post a transaction from a cash payment journal to the accounts payable subsidiary ledger.

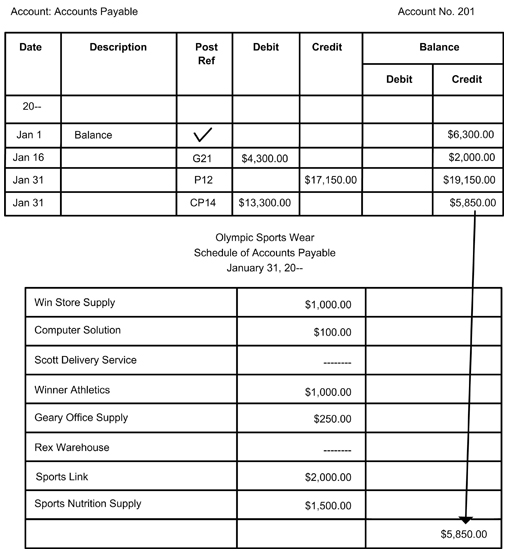

Example 2: The following example illustrates the Olympic Sports Wear account payable subsidiary ledger after all postings have been made. You will notice that the accounts contain entries from the Purchases, Cash Payment, and General ledger.

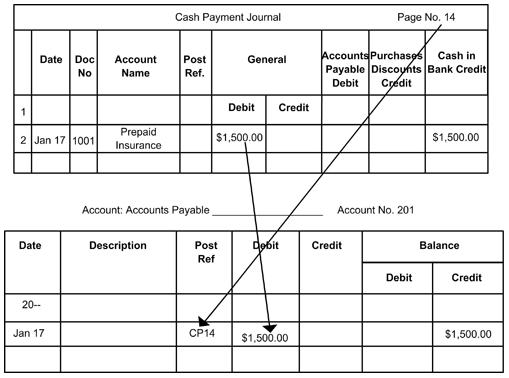

Posting Cash Payment Journal to Ledger Account

The following example illustrates an example of posting cash payment journal to ledger account.

Posting from the General Debit Column

All transactions in the General Debit column are posted to the General Ledger accounts. This is similar to the entries posted daily from the General Credit column to the appropriate General Ledger accounts.

Steps to Post from the General Debit Column:

- Enter the date of the transaction.

- Enter the journal letters and the page number.

- Enter the amount from the General Debit column of the Cash Payments journal.

- Compute the new balance and enter it in the appropriate balance column.

- Enter the account number in the posting reference column.

Totaling, Proving, and Ruling the Cash Payments Journal

The procedure to total the cash payments journal follows the same steps as other special journals. The final step is to prove the equality of debits and credits.

| Debit Columns | Credit Columns | ||

| General | $10,300 | General | $1,026 |

| Accounts Payable | $13,300 | Purchases Discounts | $146 |

|

|

| Cash in Bank | $22,428 |

|

| $23,600 |

| $23,600 |

Since debits equal credits, the cash payment journal should be double ruled.

Posting Column Totals to the General Ledger

By the end of the month, the accountant posts the total of each Special Amount column to the General Ledger account named in the column heading. For the Cash Payments journal, column totals are posted to Accounts Payable, Purchases Discounts, and Cash in Bank.

Proving the Accounts Payable Subsidiary Ledger

After posting the column total, you should prepare a schedule of accounts payable. The schedule gives information about:

- All the creditors in the accounts payable subsidiary ledger

- The balance in each account

- The total amount owed from all creditors

You should prove the accounts payable subsidiary ledger only when the following agree:

| The total of the schedule of accounts payable | = | Accounts Payable (controlling) account in the general ledger |

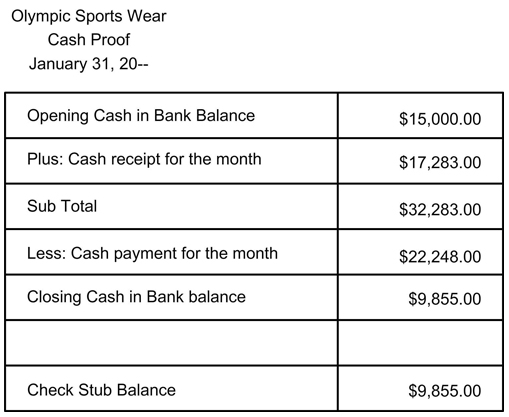

Proving Cash

The cash records in the accounting records must agree with the amount entered in the cashbook. The process of verification for the balance in the accounting records and the checkbook is known as proving cash. Ideally, businesses should prove cash each day.

Steps to Prove Cash

Step 1: Record the beginning balance of the Cash in Bank account according to the General Ledger account.

Step 2: On the next line, enter the total cash received during the month. This is the total of the Cash in Bank debit column from the Cash Receipts journal.

Step 3: Add the first and second lines.

Step 4: From the subtotal, subtract the cash payments for the month. This is the total of the Cash in Bank credit column from the Cash Payments journal.

Step 5: Compare the amount obtained in Step 4 to the balance shown on the last check stub in the checkbook.

Step 6: If the ending balance of Cash in Bank and the balance on the check stub match, you have proved cash.

Proving cash verifies:

- The amount recorded in the general ledger

- Cash receipts journal

- Cash payments journal

- The checking account balance

Note: proving cash does not confirm that the bank has processed all deposits from the business or that all outstanding checks have cleared.